The dream of owning a home is evolving. Across the United States and Europe, the rise of house kits and modular prefab homes has offered a faster, more sustainable path to homeownership. However, the most common hurdles aren’t the construction itself, but the “hidden” phases: Securing a loan and navigating local permits.

If you are looking to build a modern cabin, a backyard ADU (Accessory Dwelling Unit), or a full-scale family home using a kit, this guide will walk you through the financial and legal landscape of 2026.

1. Why Traditional Mortgages Often Fail for House Kits

Most first-time builders are surprised to learn that you cannot simply walk into a bank and get a standard 30-year fixed mortgage for a house kit that hasn’t been built yet.

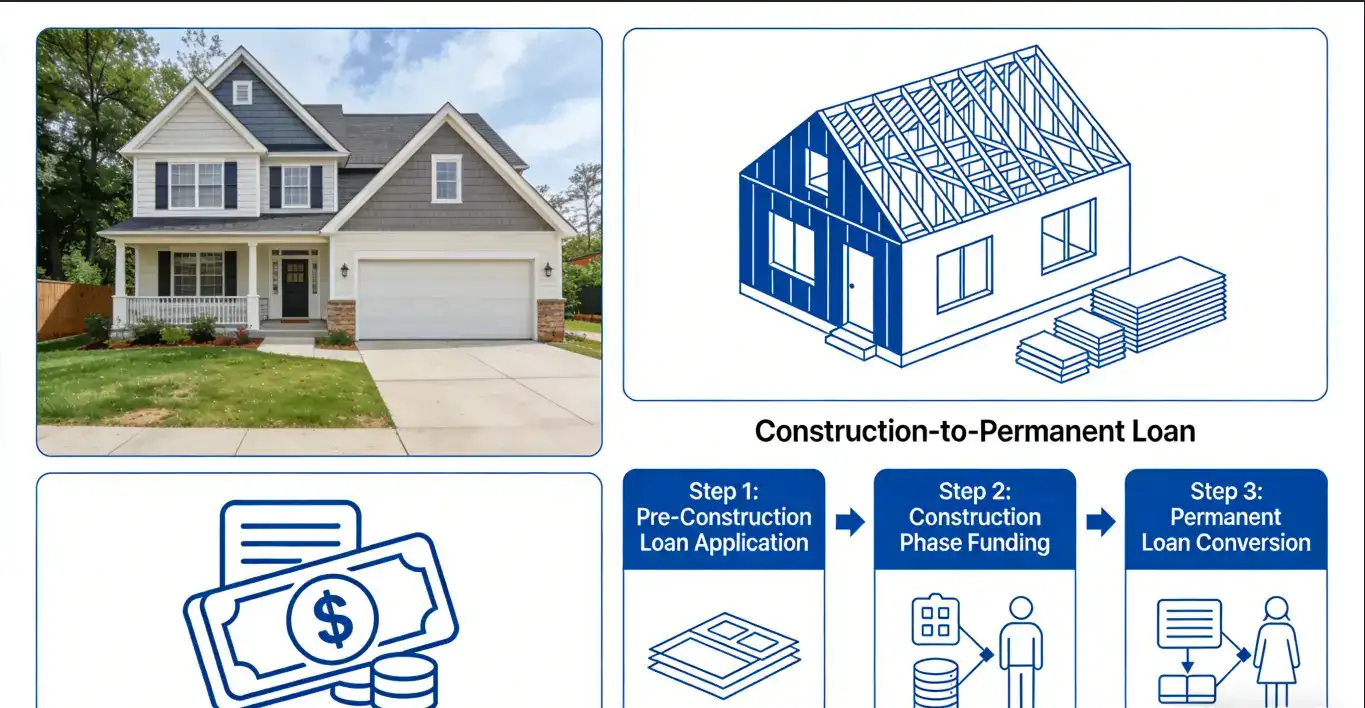

Standard mortgages require the home to serve as collateral. Since a house kit starts as a stack of materials in a shipping container, there is no “house” to secure the loan. Instead, you need a Construction-to-Permanent Loan.

- How it works: The bank pays out “draws” to your contractor or the kit manufacturer as milestones are met (e.g., foundation poured, kit delivered, roof on).

- The Transition: Once the home receives a Certificate of Occupancy, the loan automatically converts into a traditional mortgage.

2. Zoning Laws: Can You Actually Build There?

Before you click “buy” on that stunning A-frame kit, you must check your local Zoning Ordinances.

In the United States:

The trend is moving toward ADU (Accessory Dwelling Unit) friendliness. States like California and Oregon have passed laws making it easier to add a kit house to your backyard. However, you must still check:

- Setback Requirements: How far the structure must be from your property line.

- Minimum Square Footage: Some counties prohibit homes under a certain size.

In the United Kingdom & Europe:

The “Caravan Act” may apply to some mobile-ready kits, but most permanent structures require full Planning Permission. In 2026, many councils prioritize “Green Builds,” so highlighting the eco-friendly nature of your house kit can often speed up approval.

3. Budgeting for the “Invisible” Costs

The price tag on a house kit website is rarely the final cost. To avoid financial distress mid-build, budget for these three essentials:

| Category | Estimated Cost (US Avg) | Why it’s Needed |

| Foundation | $5,000 – $15,000 | Kits require a concrete slab, crawl space, or piers. |

| Utility Hookups | $3,000 – $10,000 | Connecting to the city grid (water, power, sewage/septic). |

| Permit Fees | $1,000 – $5,000 | Local government filing and inspection fees. |

4. How to Improve Your Loan Approval Odds

To satisfy a lender’s “Master” requirements, you need a Builder’s Packet. This should include:

- Detailed Blueprints: Provided by the kit manufacturer.

- A Licensed General Contractor (GC): Banks rarely lend to “Owner-Builders” without professional oversight.

- Appraisal of the Land: The value of your lot is a key part of your equity.

5. Frequently Asked Questions (FAQ)

Q: Are house kits more expensive to insure?

A: Generally, no. Once completed, if the kit meets local building codes (like IBC or IRC), insurance companies treat it like any other stick-built home.

Q: Can I use a Personal Loan instead of a Construction Loan?

A: For smaller “Tiny House” kits under $50,000, an unsecured personal loan or a Home Equity Line of Credit (HELOC) on your existing property may be faster and easier.

Q: Do house kits depreciate like trailers?

A: No. Unlike mobile homes, kit houses built on a permanent foundation typically appreciate in value alongside the local real estate market.

Final Thoughts

Becoming a House Master means doing your homework before the first nail is driven. By securing the right construction financing and verifying your local zoning laws, you transform a risky project into a solid real estate investment.

Leave a Reply